Unilever: Recession resilient business at an attractive price

Unilever, recognized for its resilience during downturns, is in the midst of a strategic transformation. As a high-quality, lindy company, it is undervalued, presenting attractive returns.

Introduction: Unilever

TL;DR

Market Cap: US$126 billion

Stock Price: US$50.47

Dividend Yield: 3.7%

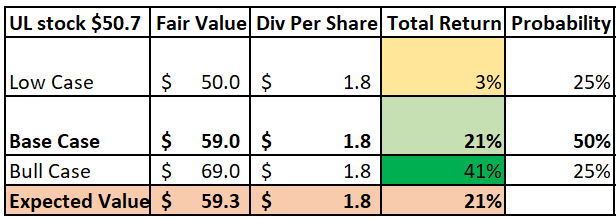

Intrinsic Value: $60

Total Return (Stock return + Dividend) = 20% [Base Case]

Basics: Unilever, with a global footprint as a consumer goods company and a century of success, touches 3.5 billion lives across 190 countries with 400 brands. It's a financial and brand powerhouse.

Strengths: Its edge? Recognizable brands, vast distribution, and massive scale. These keep Unilever integral to daily life.

Stumbles: Recent years saw missteps: cost-cutting over brand building and a failed buyout bid, hitting growth caused by bloated bureaucratic organization.

Peltz Steps In: Enter Nelson Peltz, the activist behind P&G's revival (100% stock returns from FY17 to FY22), now eyeing Unilever for efficiency, focus on growing leading brands, and organization structural simplicity.

Turnaround Signs: Signs are good. Organic volumes are up for the first time in years, margins are better, organization is leaner and focus sharpens on profitable 30 'Power Brands' - 75% of total sales

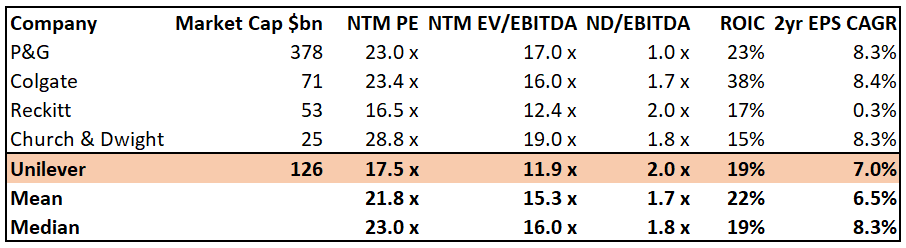

Market Mispricing: Yet, Unilever's market valuation lags (5 turns discount to P&G despite growing faster and being nearly as profitable), presenting an unmatched buy-in point, given Peltz's history and Unilever's ongoing strategic pivot.

Why Buy: With Peltz at the helm, promising a strategic overhaul akin to his achievements at P&G, Unilever is not just poised for recovery but is expected to deliver at least 20% returns. This projection is conservative, considering the transformative impact seen at P&G, positioning Unilever as a compelling investment opportunity with substantial upside potential.

Unilever is cheaper than P&G, has similar growth (consensus numbers are understated as the the new strategy is still a show me story),

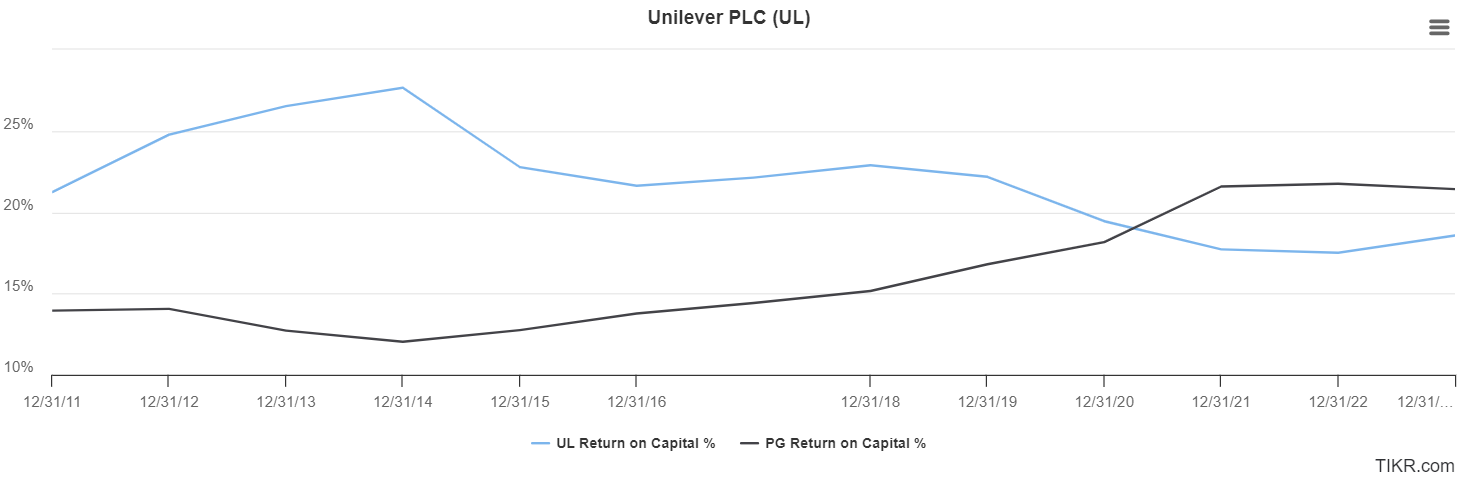

Unilever historically outperformed P&G in investment returns. With Nelson Peltz now part of Unilever’s board, an increase in ROIC (return on invested capital) is on the horizon, similar to the growth he spurred at P&G. This expected rise is NOT YET reflected in Unilever's stock price.

The reason for decline in ROIC is loss of profitability (operating profits - firm level profits) which is precisely what Nelson Peltz is focused on.

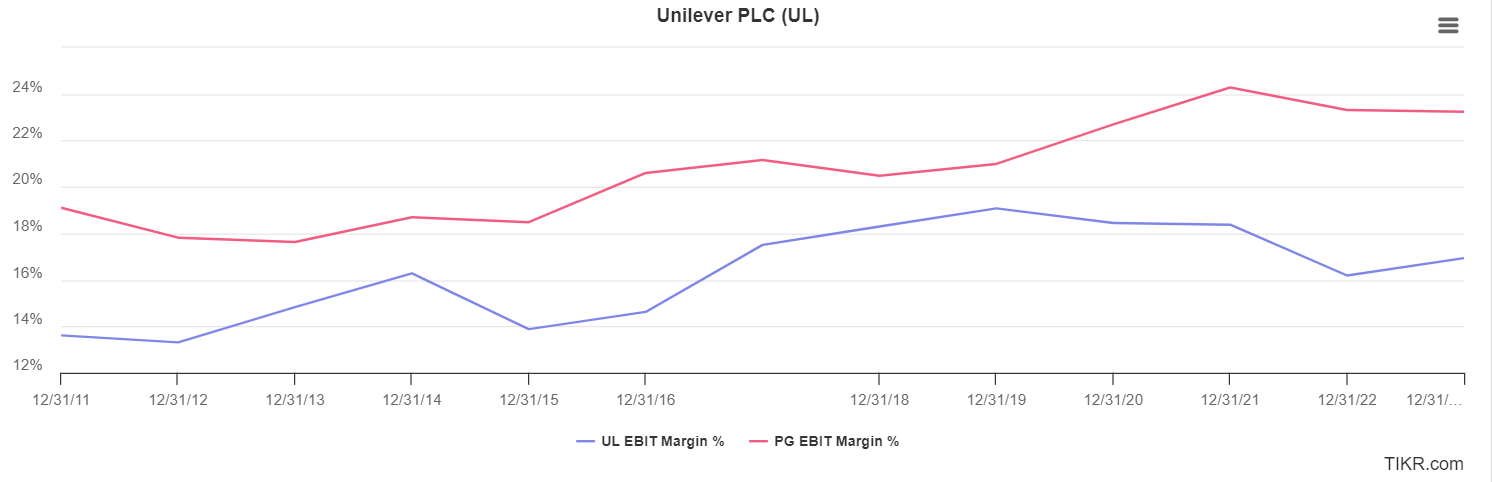

Unilever's lower margins than P&G stem from its food business, which inherently has lower margins and its significant exposure to emerging markets where inflation has sharply increased input costs. These factors have widened the margin gap. However, with inflation now cooling in emerging markets and new leadership aiming to revitalize the food business, these margin pressures are beginning to ease.

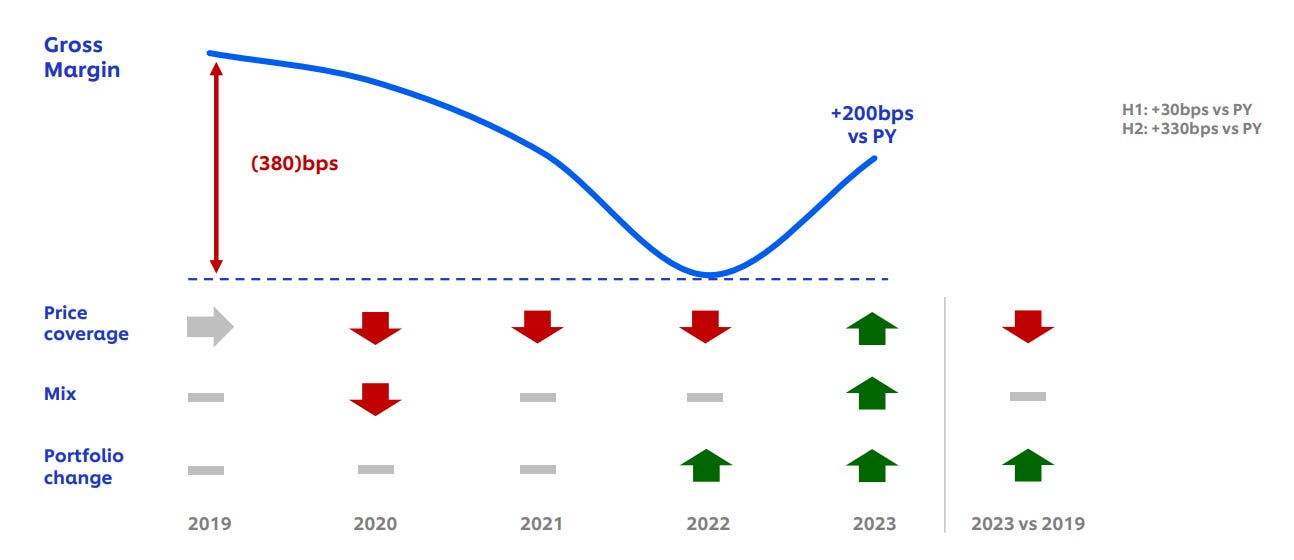

Margin recovery starting from unit level profitability (gross profit margin) is firmly underway

Introduction

Imagine walking down any supermarket aisle in the world. Chances are, you'll pass by a product from Unilever. From the moment we wake up to the time we go to bed, Unilever is there. Dove helps us start our day feeling fresh, Sunsilk gets our hair just right, a scoop of Magnum ice cream is our sweet escape, and to evening meals spiced by Knorr. It's more than just products; it's about enhancing well-being and joy for 3.5 billion people worldwide. This century-old titan, with a portfolio of 400 brands in 190 countries, boasts a remarkable track record: a return on invested capital consistently over 15% and a balance sheet as solid as they come.

Competitive Advantage: Brand, Distribution and Scale

At the heart of Unilever's success lies a trifecta of competitive advantages: unparalleled brand power, an expansive distribution network, and immense scale. This powerful combination sets Unilever apart in the global marketplace, weaving its products into the fabric of everyday life.

Brand: Unilever's foremost competitive advantage is its powerful brand recognition. The company's portfolio includes some of the most trusted and recognizable brands in the world, such as Dove, Sunsilk, and Knorr. This strong brand equity reduces search costs for consumers, simplifying their purchasing decisions and fostering loyalty. It also acts as a formidable barrier to entry for new competitors, safeguarding Unilever's market position.

Here's the scoop: Unilever nails the basics—things we use every day, like soaps, shampoos, and our favorite snacks. Why does that matter? Because when it comes to what we put on our bodies or bring into our homes, we're not exactly looking to experiment. We want quality, we want safety, and guess what? Unilever delivers just that.

Distribution: Unilever's extensive distribution network is a critical competitive advantage. By securing valuable shelf space in major grocery chains—which account for 60% of its sales channels— Unilever's distribution network ensures that whether you're in New York or New Delhi, your favorite products are just an arm's length away. This widespread distribution access enhances product visibility and convenience, further strengthening consumer preference for Unilever brands.

Scale: The sheer scale of Unilever's operations amplifies its competitive edge. With a vast array of products across multiple categories, Unilever leverages its size to achieve economies of scale in production, marketing, and distribution. This scale not only enables efficient cost management but also positions Unilever to negotiate favorable terms with retailers, ensuring prominent placement and availability of its products over competitors.

The opportunity to buy at an attractive price exists due to a series of strategic missteps and challenges Unilever has faced:

Shift to Cost-Cutting: The company prioritized reducing costs over investing in growth, hampering organic volume growth and innovation.

Emphasis on Profitability Over Brand Investment: Following the defense against a $143 billion takeover bid by Kraft Heinz in 2017, Unilever chose to pursue profitability, sidelining investments in its brands. This approach led to lost market share and sluggish growth, which the company unsuccessfully attempted to counter with expensive, sometimes ill-conceived acquisitions.

Matrix Structure Complications: Unilever's matrix organizational structure, intended to enhance global and local decision-making, paradoxically led to slower decision-making, stifled innovation, and diluted accountability, as middle-level managers had to report to both local and global bosses.

Purpose-Led Strategy Critique: Investors criticized the company for focusing too much on purpose-led strategies, like emphasizing the social purpose of products like Mayonnaise and Ice cream, at the expense of core business performance.

Failed Acquisition of GSK's Consumer Division: Attempting to buy GSK's consumer products division, including brands like Sensodyne and Advil, further frustrated investors, viewed as a distraction from fixing fundamental issues toward a business with low organic growth and high regulatory burden.

Nelson Peltz's Approach:

Nelson Peltz's influence on Unilever marks a strategic pivot towards revitalizing the company for enhanced growth and profitability.

His playbook, proven through a successful turnaround at Procter & Gamble (P&G), focuses on simplifying organizational structures, honing in on core brands, and reinvesting in emerging trends. Here's a comprehensive breakdown of the strategy and its implementation at Unilever:

Activist Investment Philosophy:

Peltz takes minor equity stakes in large companies, advocating for substantial strategic shifts towards focusing on core brands and eliminating bureaucratic hurdles, notably the matrix structure that slows innovation and decision-making.

P&G as a Blueprint: Peltz's involvement in P&G since 2017 led to significant improvements in volume growth and operational efficiency, resulting in a 100% total shareholder return from FY17 to FY22. This success underpins his strategy for Unilever.

Strategic Shifts at Unilever: New CEO, Strategy and Management [Spoiler Alert: Changes are showing positive results]

Addressing Key Challenges: Since Peltz's stake in November 2022, Unilever has focused on overcoming stagnant volume growth and the inefficiencies of the matrix structure, which had previously led to excessive costs.

Initial Successes: Unilever has reported sales volume growth for the first time in two years and margin improvements, thanks to a strategic focus on 'Power Brands'—30 brands contributing to 75% of total sales, showcasing higher margins.

Hein Schumacher's Leadership: New CEO

New Direction: With Schumacher at the helm since June 2023, Unilever has seen a decisive shift towards streamlined operations, eliminating the matrix structure in favor of clear P&L accountability across five distinct business units: Beauty, Personal Care, Home Care, Nutrition, and Ice Cream.

Focusing on Profitability: Schumacher's strategy emphasizes investing in the 30 'Power Brands' and restoring core unit profitability to pre-pandemic levels, leveraging easing commodity prices and supply chain optimizations.

P&G vs. Unilever: Unilever is marginally better than P&G

Unique Advantages: Despite historical comparisons with P&G, Unilever possesses distinct strengths, including significant exposure to emerging markets (60% of total sales) and a diverse brand portfolio. The company's strategy includes rotating its portfolio towards faster-growing sectors like health, beauty, and hygiene.

Organizational and Financial Adjustments: Unilever has undertaken massive organizational changes, reducing senior and junior management roles to improve efficiency. These changes are part of a broader effort to boost profitability and shareholder returns, including a EUR1.5 billion share buyback program for 2024.

Total Return and Valuation Insights: At least 20% total return

Valuation Metrics:

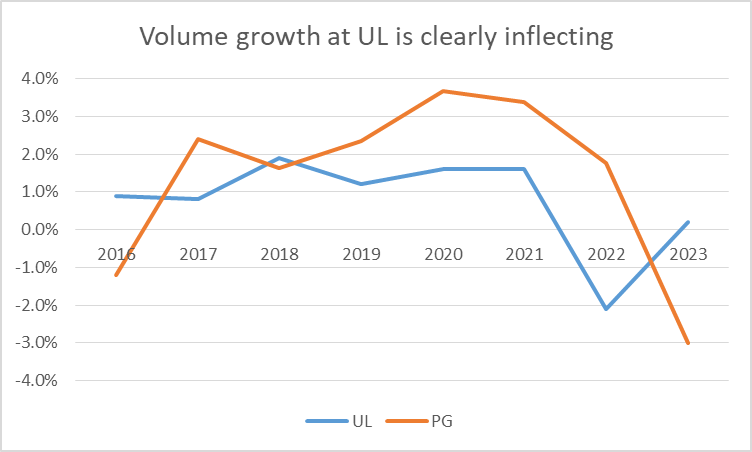

Despite expectations for Unilever to grow as rapidly as Procter & Gamble (P&G), the market remains skeptical due to Unilever's performance over the past five years. However, Nelson Peltz's strategic interventions have begun to show results, with Unilever experiencing positive volume growth for the first time in five years and a gross profit margin increase of 220 basis points.

Organizational Overhaul: Significant changes have been implemented across Unilever's structure. The most notable include the appointment of the head of the Beauty and Wellbeing division as the new CFO, the dissolution of the matrix organizational structure, and the restructuring of Unilever into five distinct business units. These units now operate with full P&L responsibility, and underperforming segments like Nutrition and Ice Cream have seen leadership changes.

Market Positioning: Unilever now offers higher earnings growth potential compared to P&G but is currently trading at a 5x discount. This discrepancy presents a unique investment opportunity.

Reverse Discounted Cash Flow (DCF) Analysis: Market expectations, as inferred from a reverse DCF, suggest a market implied modest 3.5% CAGR in earnings growth over the next decade, significantly below the long-term average of 7%. If Unilever's margins remain stable and earnings growth improves to 5%, there's a potential 20% upside, aligning the stock's P/E ratio with long-term trends. Said another way, the market expects Unilever to grow at 3.5% but is on track to grow at 5%, with a potential for 7%, leading to a very favourable skew of outcomes

Share Buyback and Dividend: Unilever has initiated a EUR 1.5 billion share buyback program for 2024 and maintained its quarterly dividend, demonstrating confidence in its financial health and commitment to shareholder returns.

Asymmetric Risk/Reward:

The current market pricing reflects a conservative 3.5% earnings growth expectation, suggesting that the downside risk is minimal. With the stock perceived as undervalued, investing at the current price offers a high-quality opportunity with a potential 20% return, supported by a solid ROIC of 15% and a dividend yield of 3.6%.

Catalysts for Growth:

Strategic Execution: Continued positive volume growth and strategic reinvestment in brands and new product developments are key drivers for sustaining profitable growth.

Potential Risks:

Leadership and Strategy Changes: Any significant alterations in leadership or strategic direction could impact the company's growth trajectory and market confidence.

Appendix:

Fair value obtained using a 10yr DCF at 9% cost of equity and 2.2% terminal growth. Base case fair value equates to 19.7x NTM PE which is inline with the long term average providing another set of guardrails for the DCF assumption.

Loved the analysis!